In volatile markets, we’re often asked “should I move to cash?” The thought process may be that moving your investment to cash, either within your investment portfolio or a bank account, means your money holds a certain value. While this may be appropriate for some people in certain circumstances, it could be the case that being in cash means you miss out on growth in an investment.

Moving your investment to could be damaging to your long-term investment aspirations. This could mean either selling assets and holding the proceeds as cash whilst remaining within your investment portfolio, or withdrawing your funds from the wrapper, to hold as cash in a bank account which may also have tax implications. The reason this could be damaging to your long-term investment aspirations is because Timing the markets is almost impossible, you don’t know when market values are going to go down or up. It is time in the markets that opens the opportunity for growth in investment value.

What is time in the markets?

Time in the markets means being invested for many years, it means not trying to predict market movements or trying to invest at the optimal time. Time in the markets allows you to potentially benefit from compound growth, where your initial investment grows in addition to growth on growth.

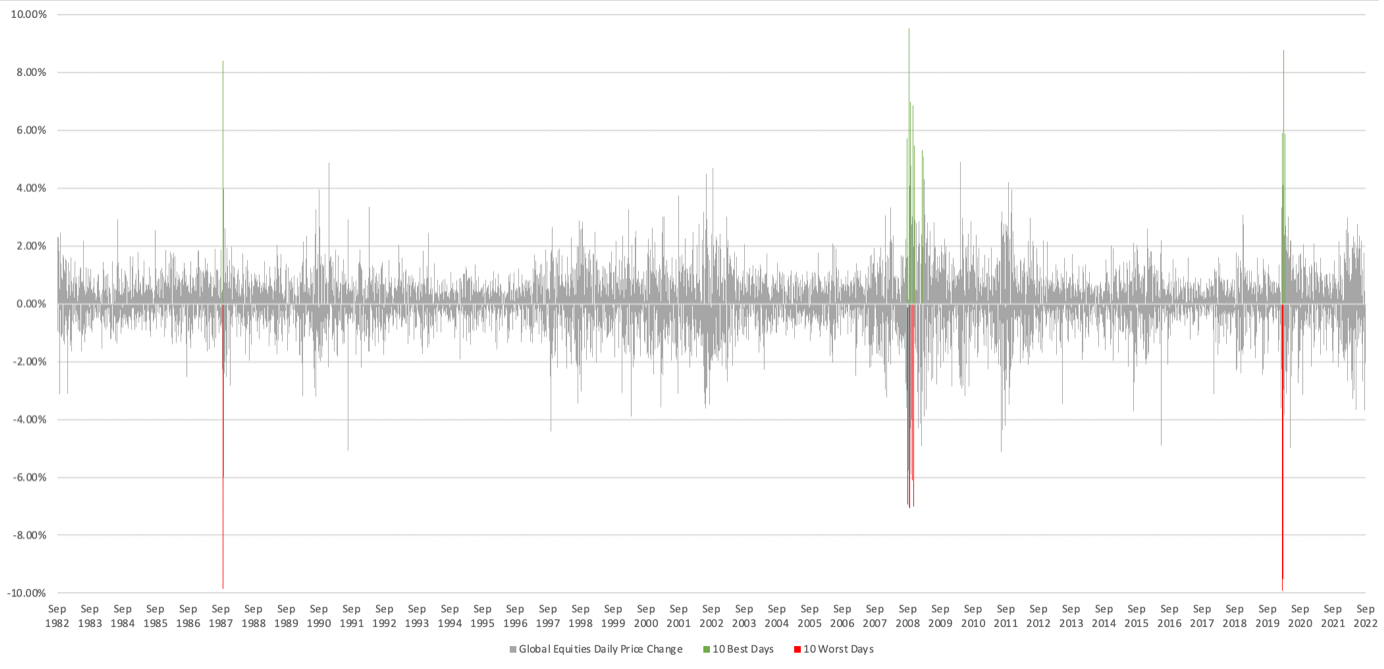

To highlight the futile nature of trying to time the markets, consider the below chart, which highlights that the “best” and “worst” days are often close together. The worst day to disinvest is in fact the best time to buy as you could get more units for the same amount of money. Staying invested can be more beneficial than trying to time the market due to potential compound growth.

Bloomberg finance 21/10/22

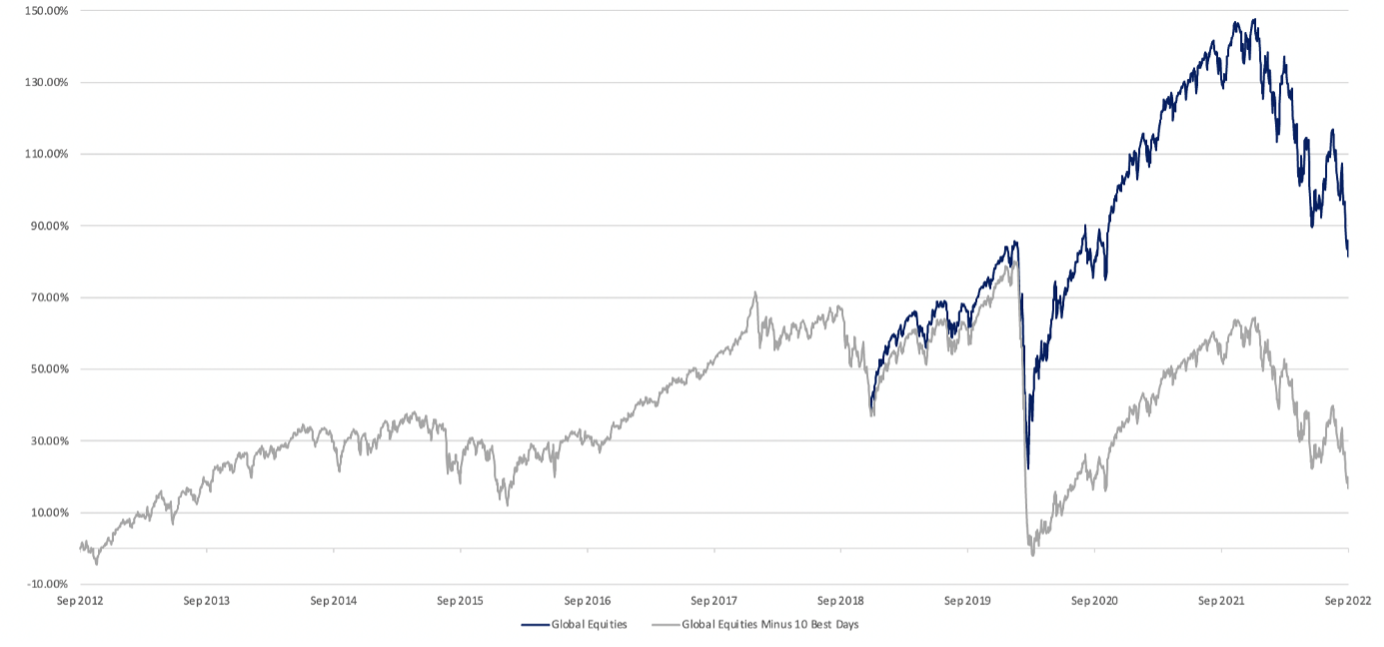

And in the following chart, look at the impact of what happened over the last 10 years if you weren’t invested for the best 10 days – it has a big impact on returns. These figures are looking at equities only, other asset types may not have had the same trajectory.

Bloomberg finance 21/10/22

In recent terms, and in the long term, you can see that being out of the market didn’t provide any benefit to the investor. Keep in mind that past performance isn’t indicative of the future.

Neil Rayner, Head of Central Advice at True Potential Wealth Management, spoke on the True Potential Do More With Your Money show about the temptation to sell assets to cash during market turbulence. This is purely his opinion and not financial advice or a personal recommendation:

“In times of volatility, remain invested. You have people who think about not being invested and whether their money is better elsewhere. Categorically, no, because it is important to stay in the markets. We also have many clients who want to put more money in during turbulent times, as they realise, they have a medium to long term goal.”

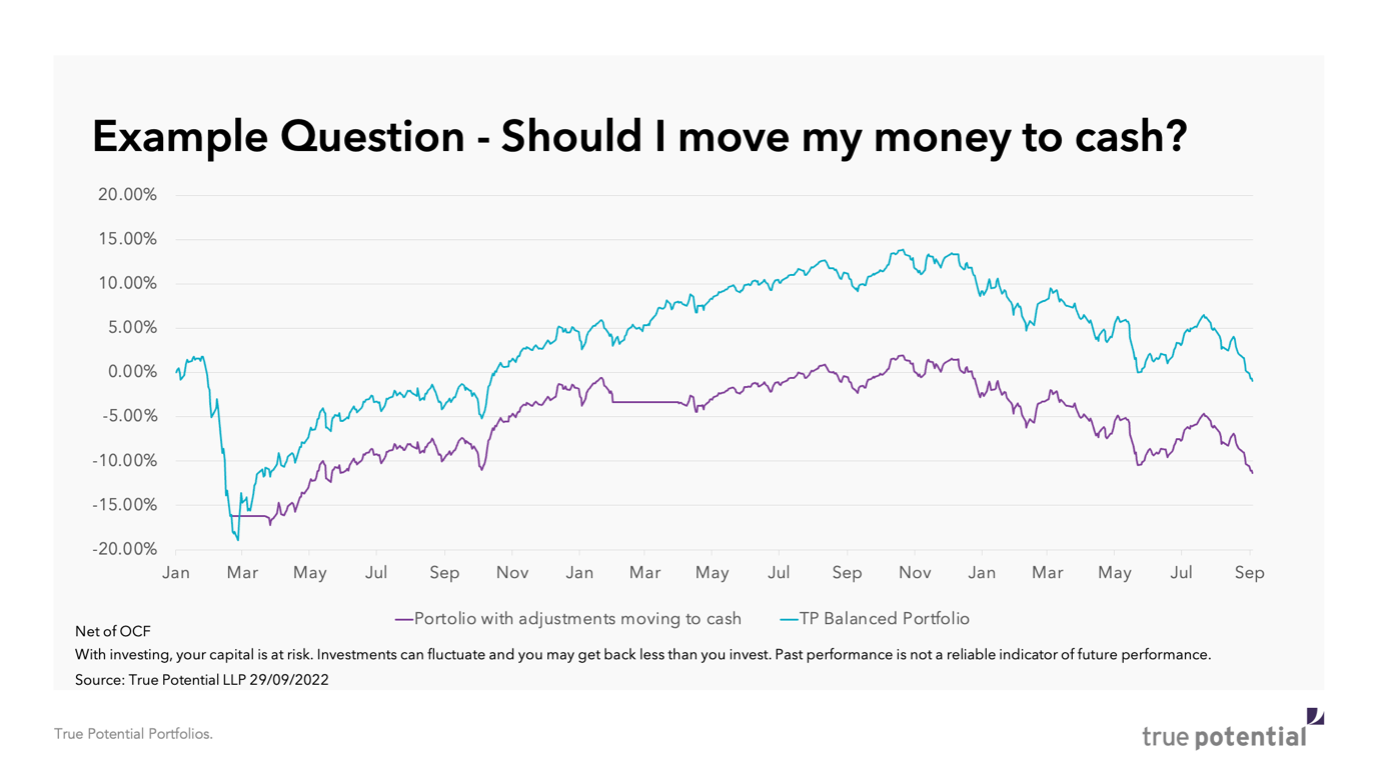

The below chart shows the danger of selling assets to cash when markets are challenged, those who ran to cash missed out on the bounce when markets recovered.

The above chart shows an investment in the True Potential Balanced Portfolio starting in January 2020. A disinvestment begins in March 2020 as the client goes to cash, hoping to avoid the volatility caused by COVID. They invest again the same Portfolio in April 2020, then disinvest and go to cash again in February 2021, returning to the same Portfolio investment in April 2021. You can see the impact going to cash had on returns in the chart.

They would have effectively been at break-even point had they done nothing and remained invested, but due to disinvesting to cash twice they are over 10% worse off.

It is worth pointing out that the TP Balanced Portfolio used in this example is for demonstration purposes only and would not be suitable for all clients.

And remember, in a diversified Portfolio, you do have some cash held through your investment. For example, the True Potential Balanced Portfolio in September 2022 holds 13.5% of cash and cash equivalents. The amount of cash within a Portfolio will relate to your attitude to risk. Generally, the lower your risk, the more cash will be held, as a client within a lower risk portfolio would usually have financial goals which mean they are willing to take less risk, in order to achieve potentially lower returns. Typically, as you get nearer to your goal, you will go down the scale from being an aggressive investor to being a defensive investor. Every Portfolio looks to grow your money, but based on attitude to risk you’ll sit somewhere on a scale of defensive to aggressive.

Chris Leyland, Director of Investment Strategy at True Potential, speaking on True Potential’s Do More With Your Money show, discussed the role cash plays in active Investment Management:

“The reality is that the Portfolios themselves have cash in there. Cash is really important within investment and the reason it is important is because you can use cash to access opportunities.”

Cash fluctuates in value

Amid market volatility, it is also important that investors remember that the value of cash isn’t certain either. There is the perception that cash isn’t a fluctuating value. T he reality is that cash is a fluctuating asset, as witnessed in currency markets, and changing inflation rates. As inflation goes higher, your cash is losing value and buying you less.

This can raise the question for investors, how much cash should you hold and what role does cash play in an investment Portfolio?

Hold an emergency fund

As an investor, it is a good idea to hold some cash. An emergency fund of cash helps to pay for unexpected costs, such as sudden household maintenance. To be clear, this means a cash holding away from your investment, such as in a bank account or accessible cash ISA. This means you have access to cash and a set amount available at any time for unexpected costs.

In terms of how much cash to hold, three months of expenditure could be a sensible amount to navigate any unexpected costs.

If you have a goal within a five-year period, it would also make sense to hold cash for that goal, as this would be too short term for investing towards.

For holding cash beyond an emergency fund and for a longer period, you could consider investing into a diversified Portfolio in a long-term investment, if this is suitable for your goal. This could give you the opportunity to grow your money beyond the rate of inflation over a longer-term period of five years or more.

Speak to a financial adviser

The best way to work out how much cash to hold, and how to think about your investment, is to speak with a financial adviser.

They can help you assess the circumstances that will be unique to you, helping you to ascertain what is the right amount of cash to hold in an emergency fund. From your disposable cash, a financial adviser can then help you to build your investment goal plan.

If you need financial advice or would like to open an account yourself; visit www.truepotential.co.uk or call our dedicated team on 0191 625 0350

With Investing, your capital is at risk. Investments can fluctuate in value, and you may get back less than you invest. Past performance is not a guide to future performance. This blog does not constitute a personal recommendation or financial advice.

Back to blog